Share this content :

Using your home as an asset can feel daunting. Paying off your loan builds equity, but it doesn’t provide quick cash. Home equity refinancing allows you to access cash, merge debt, and explore investment opportunities. As homeowners, understanding your options helps you make smart choices and start with confidence.

Table of Contents

ToggleThe Hidden Asset in Your Home

If you’ve been making mortgage payments, your home’s value has probably gone up. The difference between your home’s current market value and what you still owe on your mortgage is your home equity.

By mid-2025, U.S. homeowners had over $17 trillion in tappable equity (CoreLogic, 2025). In the past year alone, the average homeowner gained $25,000 in equity (Black Knight, 2025). Using your equity now can build your wealth even more.

Understanding Cash-Out Refinancing and Its Strategic Uses

Cash-out refinancing helps you take out a new, larger mortgage to pay off your current loan and get the difference in cash.

The cash can then be used for three main strategic purposes:

- Debt Consolidation: Pay off high-interest debts, like credit cards or personal loans, with a lower-interest home loan. This can help you save money on interest and improve your monthly cash flow.

- Home Improvements: Allocate funds to renovations that can increase your home’s value, such as updating the kitchen, bathroom, or roof. This can give you a good return on your investment.

- Financial Investment: Use this cash to buy an investment property, expand your business, or build a diverse investment portfolio.

How Much Equity Do You Need for a Cash-Out Refinance?

If you are considering a cash-out refinance, you may wonder how much equity you need to access. Most lenders require you to keep at least 20% equity in your home after the refinance. This is known as the Combined Loan-to-Value (CLTV) ratio.

For example, if your home is worth $400,000 and the CLTV limit is 80%, your total debt cannot exceed $320,000. The amount of cash you can withdraw depends on this amount.

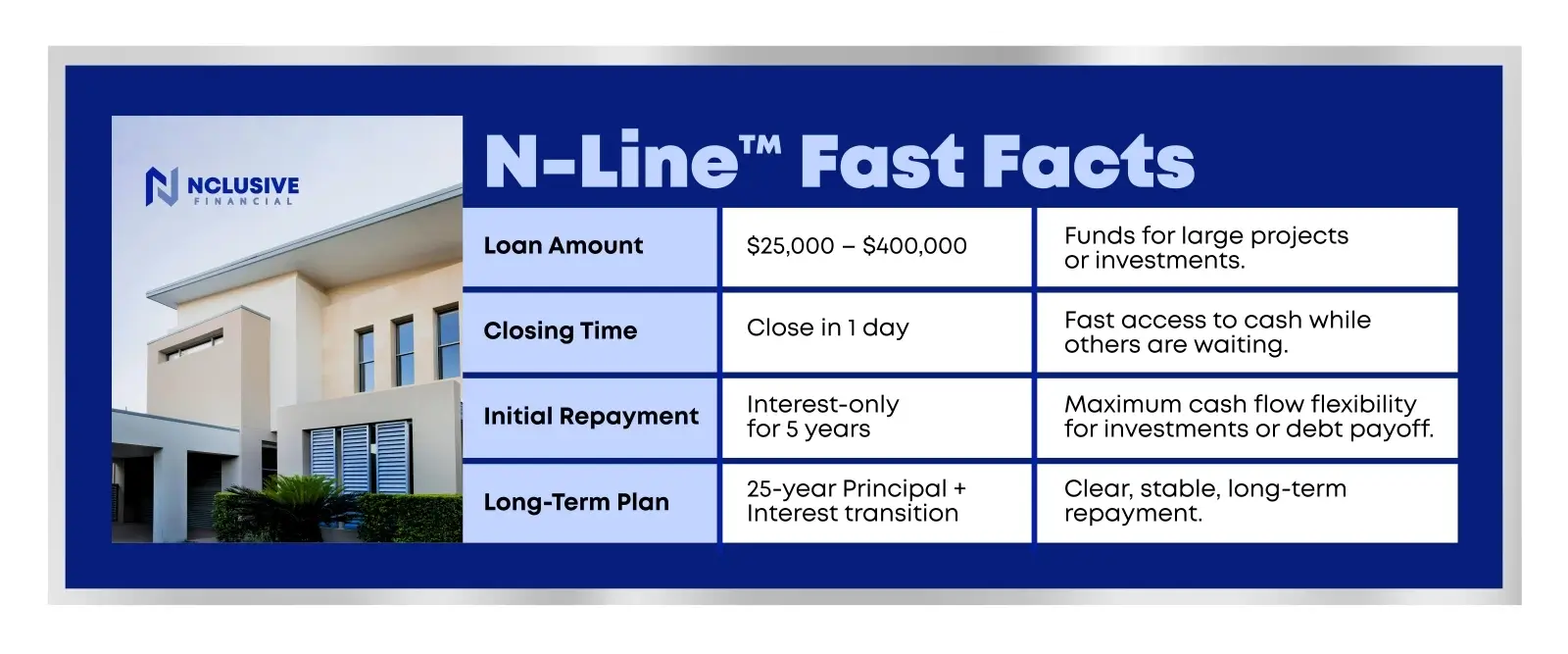

N-Line™: The Smart, Fast Way to Tap Your Equity

Traditional cash-out refinancing can be challenging because it resets your mortgage term. This means you could pay interest for longer and lose out on a favorable interest rate. Nclusive Financial’s N-Line™ program offers a better option.

N-Line™ lets you access up to 80% of your home’s value without restarting your existing mortgage. You keep your current loan, including its rate and terms, intact. Instead, N-Line™ provides cash as a separate equity loan. This way, you can improve your financial situation while keeping the security of your original mortgage.

N-Line™ provides quick access to cash, usually within 24 hours of document verification. This helps you invest or pay off high-interest debt without delay.

For the first five years, you only pay interest, which keeps monthly payments low and gives you extra cash for growth or to reduce other debts. After five years, payments shift to a regular 25-year plan with the principal and interest.

Leverage Your Home, Control Your Future

Your home equity is a valuable financial resource. With the N-Line™, you can use your property to build wealth. Shift from being a passive homeowner to an active financial planner with N-Line™. Expect fast pre-approvals, tailored loans, and trusted advice from Nclusive Financial. We’re here to help you achieve your goals. Let’s make your next move a reality.

Frequently Asked Questions (FAQs)

First-time buyers can start by improving credit, reducing debt, and learning about loan programs designed to expand homeownership opportunities. Working with professionals who specialize in supporting diverse homebuyers in real estate can also make the process clearer and more manageable.

Financial education helps buyers understand budgeting, credit, and loan options. For many diverse homebuyers, this knowledge is key to unlocking homeownership opportunities and navigating the process with confidence.

Look for transparency, education support, flexible programs, and experience working with diverse homebuyers. The right lender should actively support inclusive housing and help expand your homeownership opportunities, not limit them.

Yes. At Nclusive Financial, our N-Suite Loan Programs are designed to expand access to homeownership for buyers who may not fit traditional lending standards. These programs are especially beneficial for diverse homebuyers, including self-employed individuals, first-generation buyers, and those with non-traditional income or credit profiles, offering more flexible pathways to qualify and move forward with confidence.

Ready to turn challenges into real homeownership opportunities? Partner with Nclusive Financial Corp and take the next step to homeownership.

Disclaimer: Loans made or arranged pursuant to a California Financing Law license. We are an Equal Housing Lender. As prohibited by federal law and the laws of the State of California, we do not discriminate on the basis of race, color, religion, national origin, sex, marital status, age, because income is derived from public assistance, or because the applicant has in good faith exercised any right under the Consumer Credit Protection Act.

Key Takeaways

- Your home equity is a major asset you can access for debt payoff or investment via cash-out refinancing.

- N-Line ™ provides quick closing and a 5-year interest-only period without restarting your main mortgage.

- N-Line ™ is a strategic alternative to a full refinance, letting you keep your existing mortgage with its current rate while accessing the cash you need.

References

Black Knight. (2025). Title of Report on Homeowner Equity.

CoreLogic. (2025). Title of Report on Tappable Home Equity.

Share this content :